How Bitcoin Can Save Dying Pension Plans

How Bitcoin Can Save Dying Pension Plans

It's not yet too late

It is no surprise to anyone, that public and government pensions are dying.

For the first time in human history, we are about to have more people drawing from pension plans, than those who are paying into them. Making them nothing more than a glorified, government run, ponzi-scheme.

A Brief History

While some of the earliest promises resembling a pension stem from the US Revolutionary war, it wasn’t until Prussian progressive leader Otto Von Bismark, signed into law his Old Age and Disability Insurance Bill of 1889 that we saw the worlds first public state run pension plan.

The premise was simple:

The average working Prussian lives to be 70.

When you are working and able, you will pay into the pension via a tax.

The government will also contribute a bit to this pension, but it will underwrite the costs and pay to insure the pension.

Since the population is growing, there will be more people paying into the system than are withdrawing.

Since most people own their home, have very little debt, and have strong savings, this system is a safety net.

As a society, we can insure that we have a safe retirement both as individuals and as a collective.

This was a great system, it was adopted all around the globe, and quite frankly, it worked really well - for a while…

Jump cut to the modern era.

The average life expectancy has increased to 80-85 in most ‘First-World’ and ‘Western’ nations.

The retirement age remains at 65-70 depending on field.

The birth rate in the US has dramatically declined.

The average retiree in the US has $35,000 worth of debt still to pay off when they finish working, and does not own their own home.

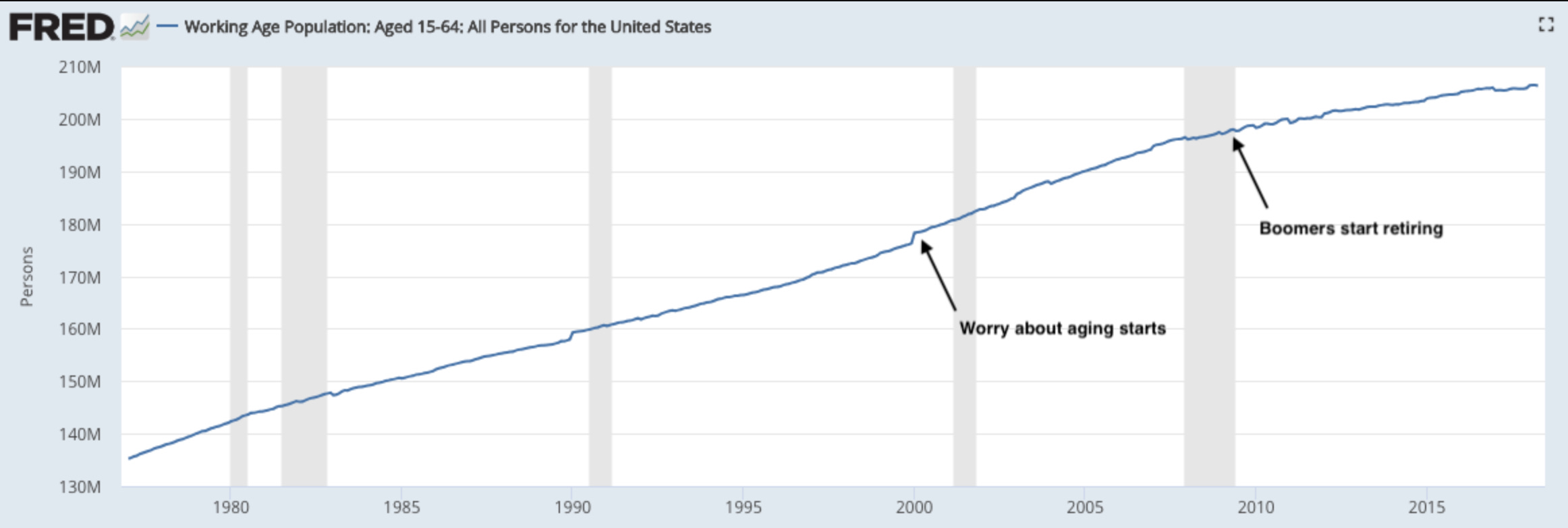

We’re about to have less people working, than are retired.

Most pensions aren’t running out quite yet, in fact estimates are that the current scheme can last until 2050.

But, that’s when things get ugly.

Right now, in the US, it looks like we’re actually at the largest ever working population - which is true. But, that’s because the ‘Baby Boomers’ are working until later in life than any generation (it’s the same reason new labor entrants are having such a tough time getting jobs.)

As they start to retire, we’re going to see a massive decline in the working population, meaning for the first time in history we’ll need to support more non-working people than working people in our economic system.

What does this have to do with Bitcoin and Pensions?

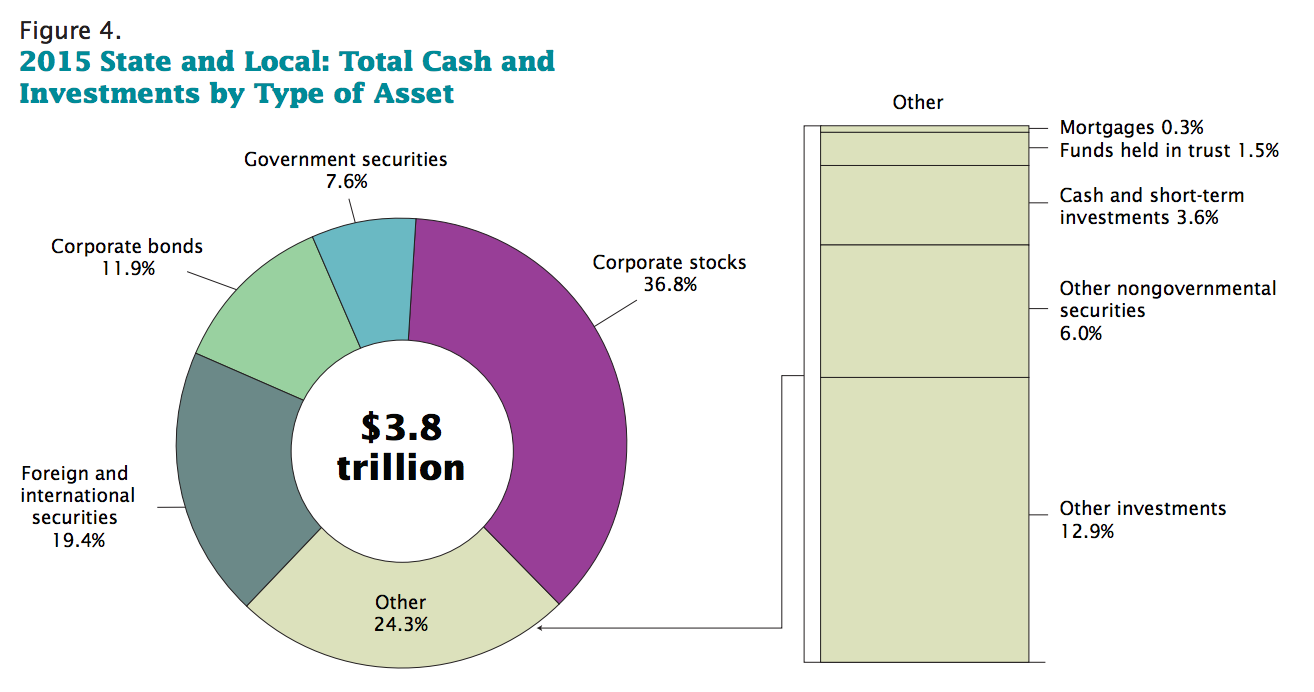

In the last full audit (2015) of state and local government pensions, it was found that the US pensions had roughly $3.8T in assets, and an average annual return of roughly 3.6%.

By nature of pensions, they have to keep their investments low-risk, and their exposure to high risk assets to a minimum. This is why the produce such a small return, by government pension standards a 3.6% yield annually is considered moderate performance.

You’ll notice a category called “Other nongovermental securities” taking up 6% of the investments in state pensions - this is usually the section that accounts for some of the more high-risk assets that an investment fund will hold, and no single asset can make up too much of that portion.

The Case For Bitcoin

If in 2015, the state pensions had taken 5% of that 6% set aside for “Other nongovernmental securities” (a.k.a 0.3% of their overall assets) and invested that in Bitcoin, then the pensions overall return would have been 19.20% annually.

More than 5.3x the current return of 3.6%.

That overall rate of growth, over the past 4 years would have amounted to around 171% yield, almost doubling state pensions from $3.8T to $6.5T in that time.

Now, we can argue semantics that such a rate of return isn’t possible because that amount of capital dwarfs the market size - but, as we’ve seen with Bitcoin in the past, every large buyer that enters the market causes a bull-run, which in turn provides more widespread awareness and adoption.

An Actual Solution?

Does this mean that pensions can simply invest in Bitcoin and be fine forever? No.

What it does mean is that by being accepting to a new emerging asset class we can provide a safety net to pensions while we continue to figure out the next steps, or when societal changes lead towards a return to population growth that will allow the model to work again.

This article is part of Coffee&Coin, a free weekly newsletter about the blockchain industry. Coffee&Coin focuses on providing editorial commentary on economic, political, legal and technology news related to blockchain technology and cryptocurrency.

Sign-up today and never miss the latest updates!

Want to follow us?

Coffee&Coin on Reddit

Coffee&Coin on Facebook

@AdamSCochran (Editor) on Twitter